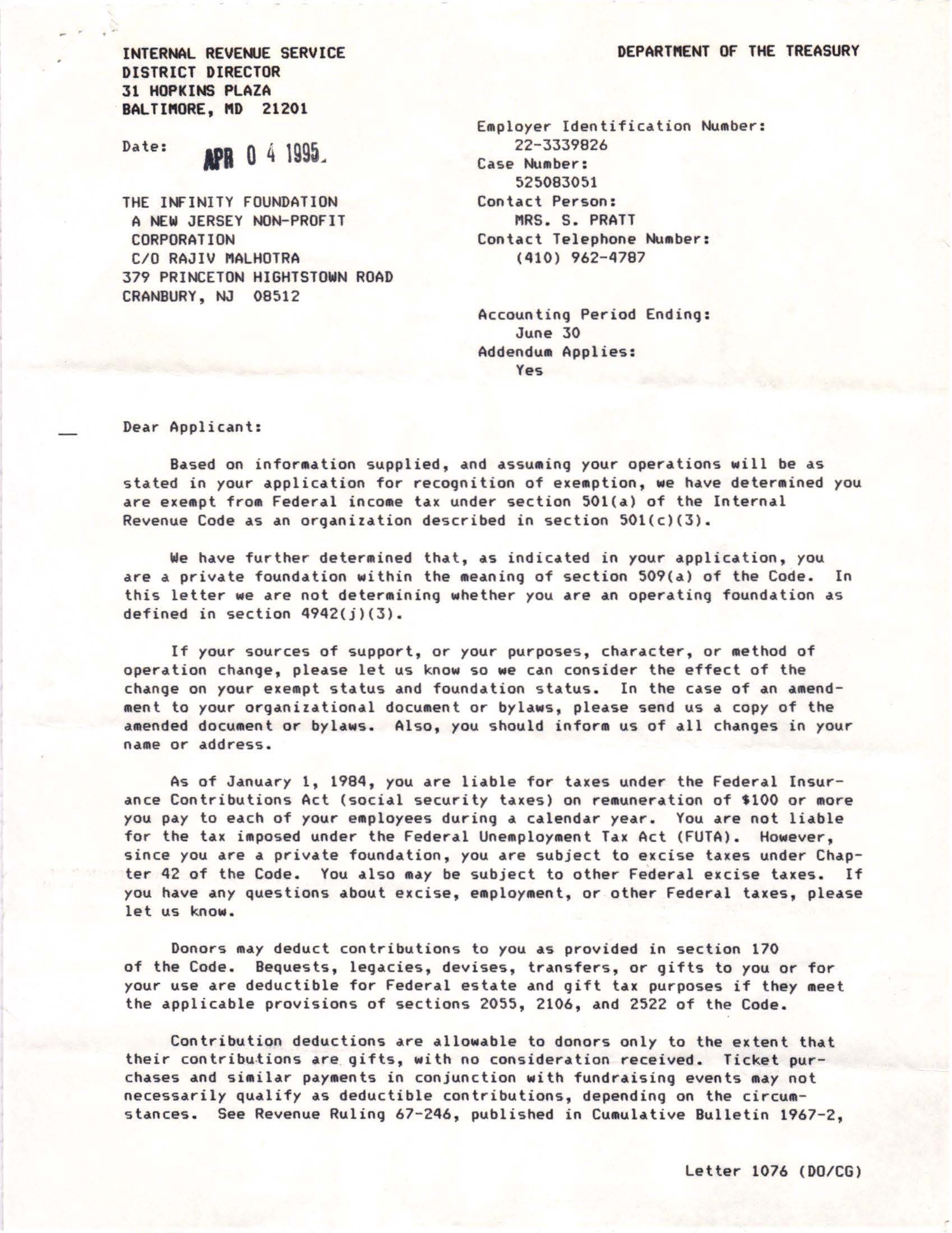

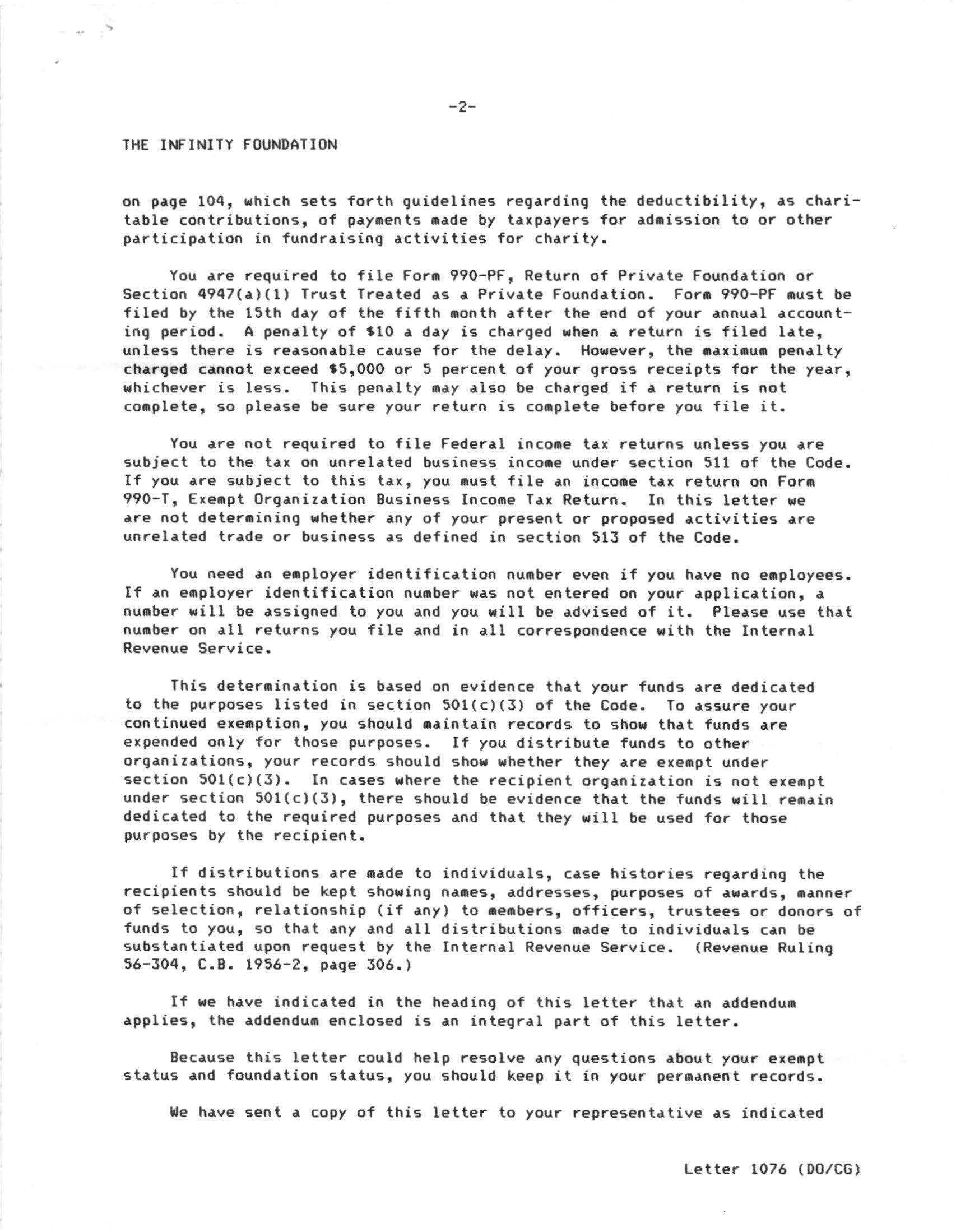

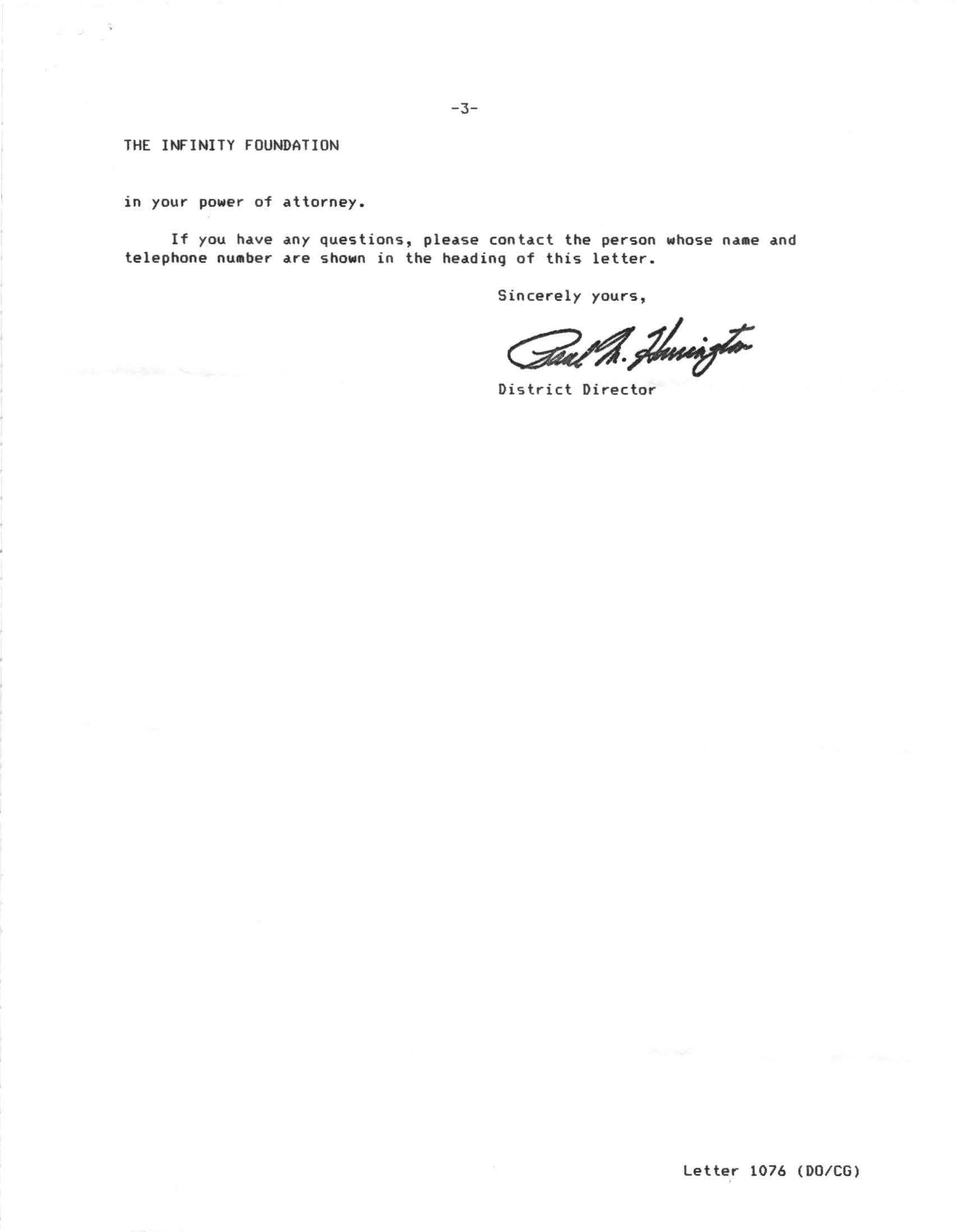

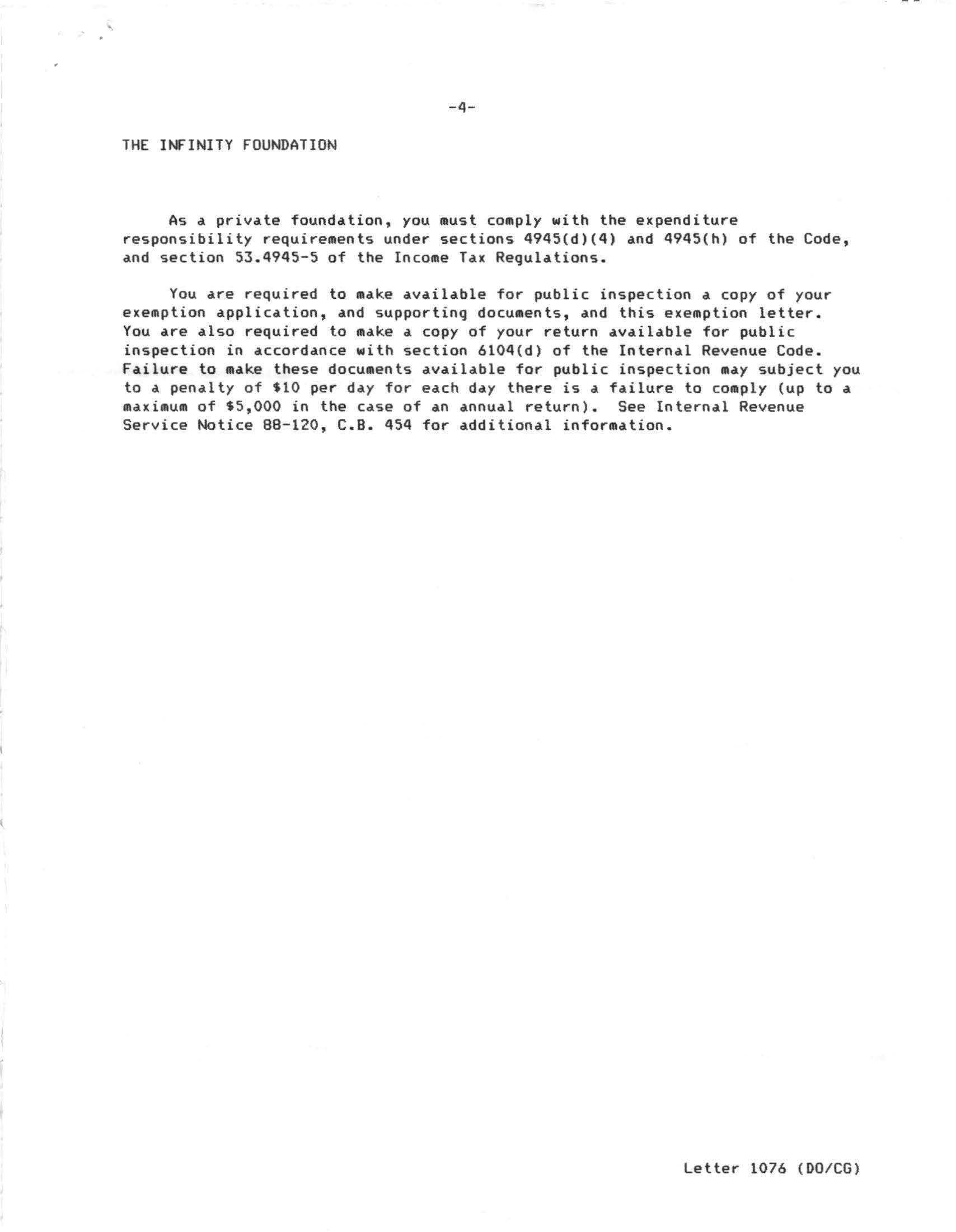

The Foundation is a registered 501(C)3 Nonprofit organization that is treated as a public charity by the Internal Revenue Service. The Foundation is also a registered Non-profit charitable organization in the State of New Jersey. Infinity Foundation is a non-profit organization based in Princeton (USA), focused on research and education. It specializes in the field of civilization studies applying the Dharma lens to examine a broad range of topics. It disseminates its unique research findings through books, videos and public events.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.